Dark Days

Few sectors of Canadian ag are as consolidated and opaque as the grain trade. In a saga that is only now coming to light, the past decade ushered unprecedented financial pain across the industry.

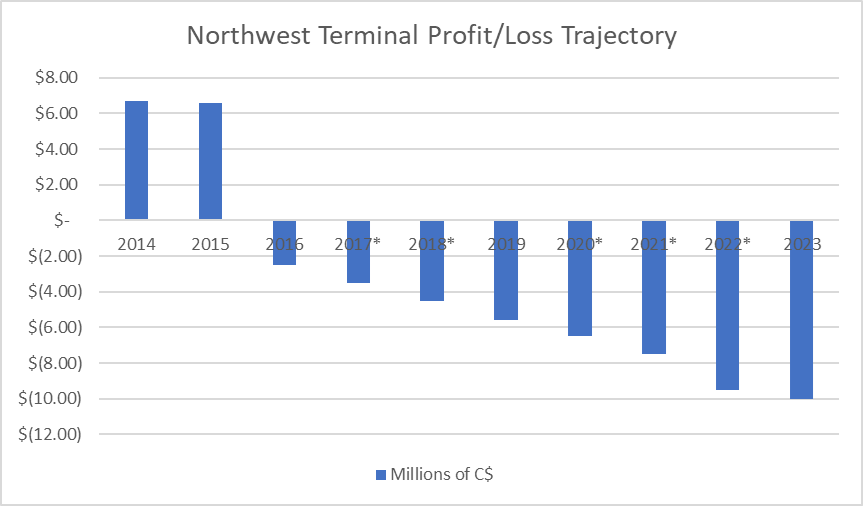

This week, a series of articles in the Saskatchewan media exposed the shock and dismay of the shareholders of Northwest Terminal, an independently-owned grain elevator. Steep losses appear to have paralyzed the Board and management team, gutting the finances of this formerly well-regarded and profitable business.

This past March, soon after parent company Above Foods’ newly-listed share price tanked, their grain origination subsidiary Purely Canada filed for bankruptcy. When the creditor list was published by the Court of King’s Bench in Saskatchewan, folks in the trade could not recall any other blowup leaving as much owing to farmers and agribusiness.

Over at the older, much larger grain companies, the fallout has been externally visible in the form of employee layoffs. Established family-run line companies have more resiliency than newcomers in bad times thanks to:

Private ownership;

Diversified offerings, in crop input sales and financing, in addition to grain trading; and

Centuries of experience and family wealth;

Looking Back

When the government of Prime Minister Stephen Harper ended the Canadian Wheat Board’s (CWB) monopoly in 2014, the party started for grain companies in western Canada. Somewhat unexpectedly freed, all of the existing and a bunch of new grain traders came on the scene, competing to buy grain.

Already by then, the lack of profitability in wheat production in the Prairies had spawned investment in local processing and crushing of the increasing supplies of canola and pulse crops. Suddenly, all of these thriving businesses could dabble in wheat and barley, too.

It’s important to note that deregulation of the CWB happened shortly after two other important and related world events:

The similarly-structured Australian Wheat Board (AWB) monopoly had already ended; and

The Arab Spring uprising, which was related to grain shortages, had destabilized North Africa and the Middle East.

New Entrant-Thinking

New investments eventually more-than-solved longstanding bottlenecks in western Canada’s grain supply chain: export capacity at the Port of Vancouver, and rail loading efficiency in the countryside. The money came from overseas grain trading companies, and sovereign wealth with new goals around long-term food security.

Increased competition for farmers’ grain came onstream gradually… and as it cyclically will do… overbuilt the handling sector leading to negative margins. These cycles used to last 3-5 years in the grain industry, but right now we’re going on 7-8 years of consistently negative grain handling margins… and discovering the end of the cash flow runway for the least resilient companies.

We pieced this chart together based on the data implied by the shareholder quoted in the article, and estimated losses in other years (marked with a *), to come up with $40mln in accumulated debt. Could this be a bellwether of the current macroeconomic situation across Canada’s grain trade? If so, expect less competition in buying grain in the future.

Diversity Pays Off

The established grain companies saw an opportunity a long time ago to diversify their business dealings with farmers, adding fertilizer and crop input sales to country grain offices. Purchase financing and bundling programs added further ways to attract farmers’ business, and challenged the comparison of prices between companies.

Other companies have taken a simpler approach and tried to compete only on grain, and only for Canadian crops that trade in big volumes globally, like wheat, soybeans, canola and peas, whose prices are all closely linked to U.S. commodity grain futures. The problem now and going forward, is that U.S. commodity grain futures are newly vulnerable to prolonged heightened volatility and weakening demand, because of:

Trump tariffs and extreme uncertainty;

Sketchy biofuel policies, i.e. that don’t deliver the intended public benefits;

Copious cheap grain exports funding Russia’s military campaign;

Unchecked expansion of corn and soybeans in South America; and

Extreme weather events.